to cutting-edge cards with guaranteed cashback,

and more

and more

Virtual — instantly: few taps and card is ready.

Pay online and wherever are supported!

![]() Funds are safeguarded and protected

Funds are safeguarded and protected

![]() We are FCA regulated institution

We are FCA regulated institution

Imagine a world without trees. We can’t.

We are thrilled to announce the launch of our new initiative in support of forest restorationS, in collaboration with the Priceless Planet Coalition by Mastercard. Now, you can make an impact on forest restoration projects with just a few clicks directly from your personal web panel or Mobile App.

Seamless payments in US dollars are now available

We are happy to announce the launch of our new payment solution for personal accounts. Now, you can send US dollar payments to most countries worldwide. Make seamless payments: the cost is 35 euros for amounts not exceeding 50,000 euros in equivalent, and 90 euros for larger payments.

Cashback for Business

Today we are launching our long-awaited cashback feature for business customers. Receive up to 0.8% on purchases with your Bilderlings card. Read more..

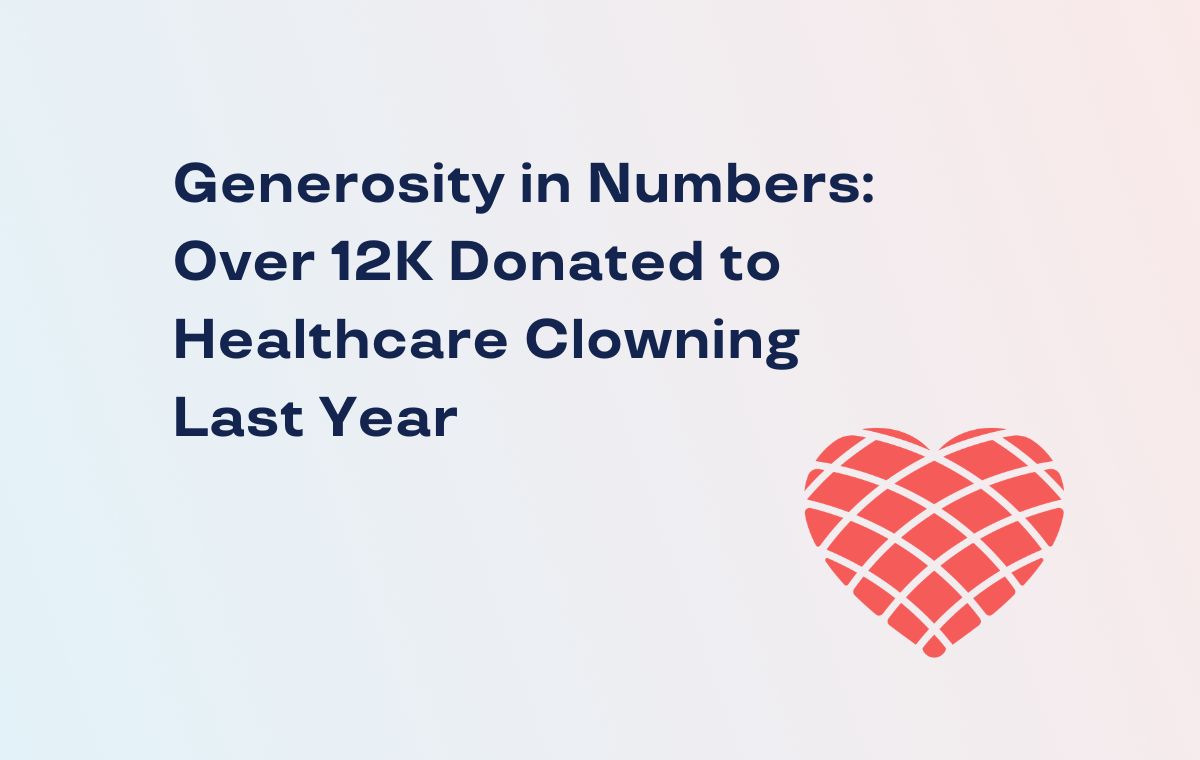

Our Clients Donated Over €12K

€12,389 has been donated using our In-App Donation Solution to support healthcare clowning. Learn more about other outcomes of the Saving Smiles project, which helps children in hospitals in the UK and Latvia.

Meet Us at TES 2024 LIS!

This February 24-27, don't miss the chance to connect with our dynamic team at TES 2024 LIS. Visit us at Booth 45 for a deep dive into thrilling affiliate business opportunities. See you there!

ICE London 2024

Mark your calendars for February 6-8, as we head to ICE London 2024, the leading event in the gaming industry. This is your perfect chance to network and get the inside scoop on the latest trends. Let's connect and explore the future of gaming together.

QR Code Payments are now available

We have successfully launched a major and highly beneficial feature: QR Code Payments! Available to all users of the latest version of our mobile app.

Free Virtual Cards in USD and GBP

Yes! We did it! Virtual cards in USD and GBP are now available. Get your new free card in your personal web panel or mobile app.

Free Account Opening for UK/EU Companies

Opening a corporate account is now free – we’ve waived the opening fee for local businesses! We believe that financial freedom should be accessible to everyone!

Save on Chinese Yuan payments

Take advantage of outgoing payments in Chinese Yuan, now available for a reduced fee of just EUR 20. Incoming payments are free!

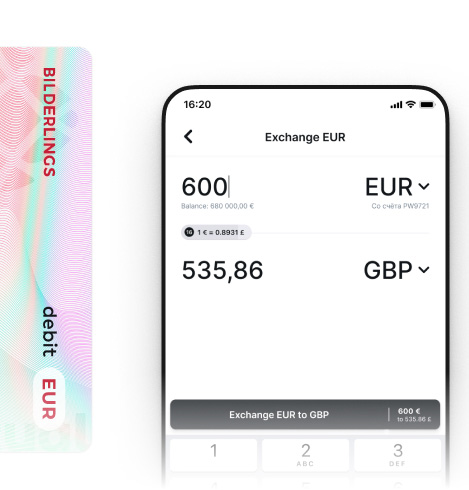

Currency Exchange 24/7

No matter where you are and what time is – you can now easily convert money all day long 365 days a year!

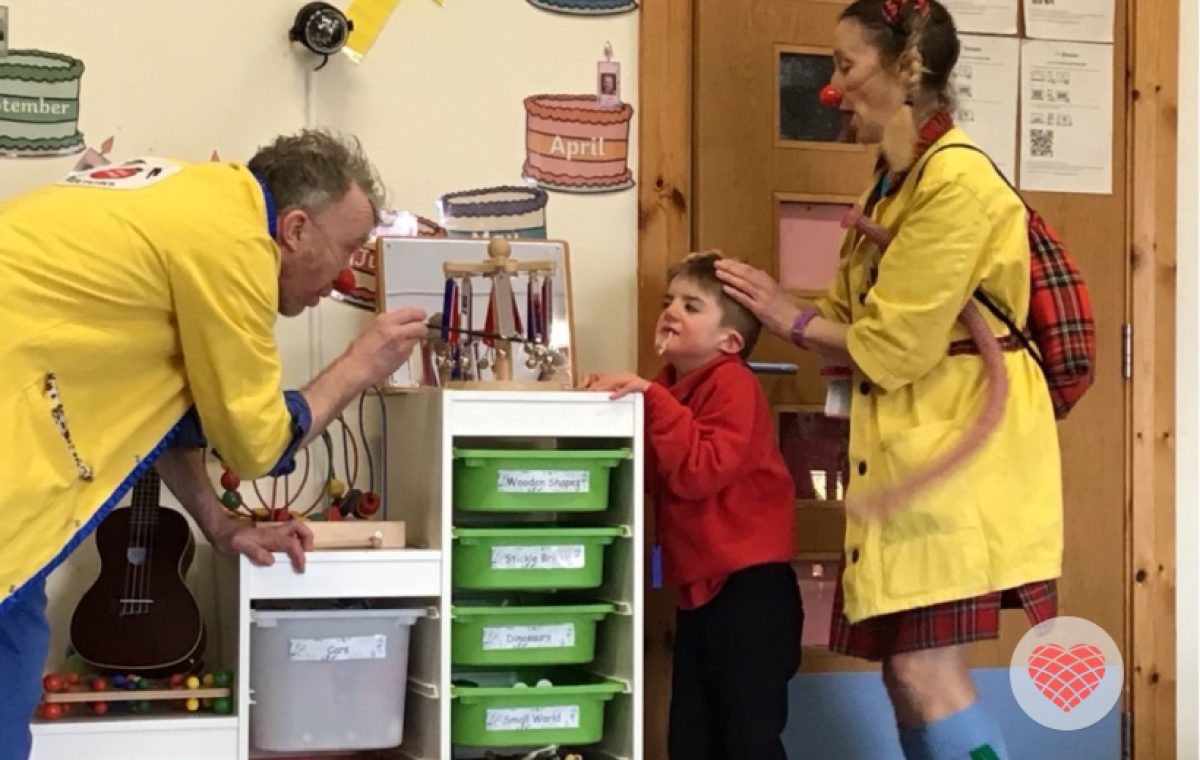

App Charity Donations Service

We launch In-App Charity Donations Service to support healthcare clowning. With just two clicks and less than five seconds, our customers can now easily support charity organizations by donating straight from their own accounts.

Fee cancellation

Starting from October 1st, we are waiving the account opening and maintenance fees for all individuals. We believe in inclusivity, and we think financial services should be accessible to everyone!

Multi-signature

Announcing multi-signature feature: a new tool now available to secure your transactions. Eliminate human error, ensuring peace of mind in your transactions.

Chinese yuan are now available

Save on Chinese Yuan payments with Bilderlings! Outgoing transactions in China for only 20 EUR, incoming payments are free of charge. Expand your horizons on the global stage.

Recurring Payments are now available

Bilderlings has launched a new feature – Recurring Payments! Make Recurring Payments automatically without having to enter data every time. Set up Recurring Payments and save your time.

We have published our annual strategic report

Read about our goals, challenges, achievements and figures. The report also includes an interesting market overview and how we are implementing AI-driven innovations to further democratise the financial industry.

GBP transfers are now available

We are happy to announce that domestic transfers in British Pounds are now available. You can send and receive funds within the UK easily now!

Google and Apple Pay has launched recently

We're delighted to announce that we've just launched the ability to add all our cards to Apple and Google Pay for all our customers worldwide!

Cashback works with smartphone purchases too!

Bilderlings becomes a SWIFT member

Bilderlings has become a full member of the SWIFT system along with the largest banks in the world. Direct integration with the SWIFT system will simplify the work with international payments for customers.